Deal Abstract

Startup creating a ‘third way’ between delivery and in-store restaurant. Has the hypothesis that it can grow customer demand for restaurants by giving customers an option to pick up their food (what they call ‘virtual drive-through’) Charges nothing to customers and relatively less to restaurants.

Shoutout to Jignesh for the tip!

Interested in startup investing? Subscribe to my premium newsletter, Startup Investing, to receive weekly content, exclusively tailored to accompany investors in their venture journey.

Decision

Passing on the deal.

Why Investing/Passing

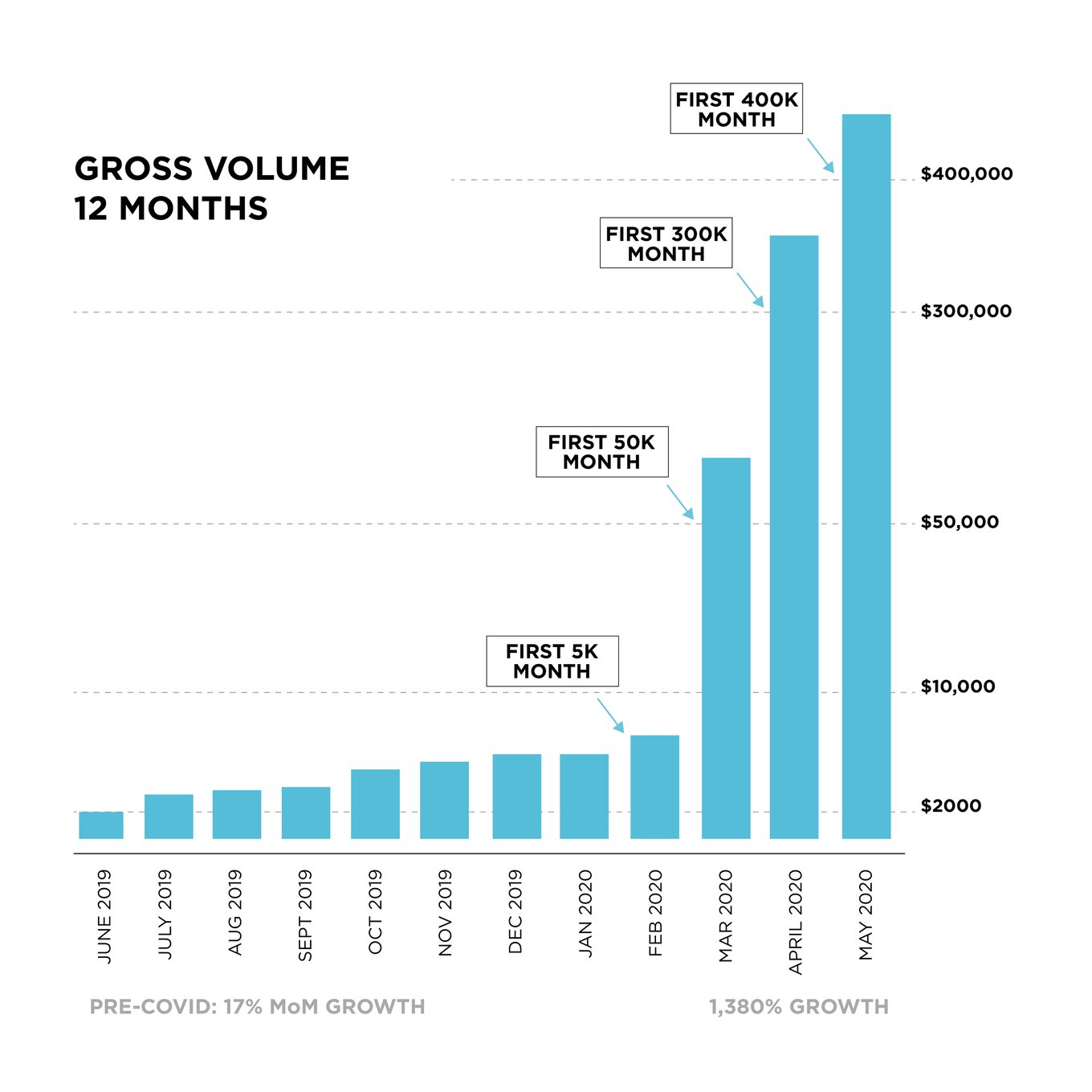

- Valuation Too High: Feb revenue $315, March rev $3150, April rev $18900, and May rev $25,200. Assuming maintaining of this, that means buying $300k of revenue/year at $12MM valuation. Compare to Contiq.

- Concerned About Whether the Business Model Works: It seems like Grubhub/Seamless charging their high rates of 35% is both predatory and also necessary. I suppose once Swipeby builds a moat, it can raise processing charges higher to 10% and still beat the 35%. But at that point, would restaurants

- Decrease in 2019 Revenue, No Learnings: Makes me concerned this will happen again in the post-COVID world.

Lots of good things going for it, but going with gut. The point of deal memos is to trust one’s gut through practice and recognizing bias.

The 6 Calacanis Characteristics (91 161 18)

| Check | Yes/No |

| 1. A startup that is based in SV | No: Winston-Salem, NC |

| 2. Has at least 2 founders | No: 1, but has 3 W-2 employees according to financial statements |

| 3. Has product in the market | Yes |

| 4. 6 months of continuous user growth or 6 months of revenue. | No: Revenue dropped from $8521 (2018) to $4569 (2019.) |

| 5. Notable investors? | No: Accelerator and private equity money. |

| 6. Post-funding, will have 18 months of runway | No: 2019 burn was $350k representing ~$30k/mth. |

The 7 Thiel Questions (ETMPDDS)

- The Engineering question:

- Big Philosophical Questions: Do big sales/too much sales make restaurants build drive throughs, or do drive throughs attract business? If the former is true, then dying restaurants without customers willing to pay for pickup are going to die. (Why wouldn’t customers just order ahead for pickup? It’s inefficient, but costs the restaurant nothing. Is it the mobile ordering value?) If the latter, then this the answer is 10x for sure since ‘virtual drive-through’ can be deployed significantly faster and cheaper. Also, using smartphones to check where customers are parked so they can be delivered is smart.

- The Timing question:

- Good: If there’s any time to be in this business, COVID would be it.

- The monopoly question:

- Good: Can scale very quickly, with set up taking 24 hours.

- The people question:

- Good Not Great: Team seems fine but nothing notable in work experience that I recognize.

- The distribution question:

- Not Great: No inside relationships with key restaurant brands that can scale them. Working with Performance Food Group (PFG) is interesting, but not proven yet.

- The durability question:

- Bad: Beside the fact that competition is pretty straightforward (and you wonder why a PFG doesn’t build this in-house? If the technology is straight forward, putting a $1MM investment to save 4.5% transaction fee for all investments seems promising.) I see this app being popular as long as restaurants temporarily become distribution centers during COVID. If this becomes the new normal, then what happens when restaurants shut down their retail premises and move to the cloud kitchen future?

- *What is the hopeful secret?:

- Can get to $2M (>6x it’s current ARR as of May) in revenue by end of 2020. 2019 revenue was $4569 for the year. “In May 2020 we passed $20K+ in net-revenue, surpassed $100K weekly GMV, and acquired 10K+ new users.”

What has to go right for the startup to return money on investment:

- 6x then 250x Revenue: Wants to process $22m transactions by end of year (6x growth) and which means $1M annual revenue. Not ARR.

- Even in the COVID New Normal, Restaurants Keep Retail Stores: This business model hinges on the assumption that restaurants won’t shut down as they realize the unit economics don’t make sense and commercial leases are killing them.

- Grow the Pie: I concur that predatory businesses like Grubhub and the like are taking too big of a transaction. That said, if that’s the revenue they needed to grow to their level, then Swipeby needs to show some way to get revenue in similar veins, while also not growing their costs.

What the Risks Are

- No Market, After COVID: “Pre-COVID-19 we saw 17% MoM growth in orders.” Looking at 2018 and 2019, this seems factually false. So, if growth is only COVID, what happens post-COVID? What did we learn from the stagnant growth in 2019?

- Capital Risk: At present only at 6.5 months of runway.

- Doesn’t Grow the Pie: Back to thesis of do driveways demonstrate restaurants with too much demand, or do driveways generate demand?

Muhan’s Bonus Notes

First time I’m seeing financial documents on Republic. It’s not a great experience. Specifically, it’s a pdf and not a searchable one, so you have to digitally sift through documents like a plebeian. That said, numbers > nothing.

Financials (References)

- Current Fundraised: $190k

- Valuation: ~12.5MM

Updates

This is where I’ll post updates about the company. This way all my notes from offering to post-offering updates will be on one page. Also, somewhat of a dearth of materials (whose the team? where are the comments? why are the financials so opaque?)